Operational Control — Definition and GHG Accounting Context

Before a single emission factor is applied, every inventory makes one decision that silently sets its total: which operations belong inside the boundary. Operational control is the most common answer to that question — and the one most often applied without checking what the standard actually requires.

Get the boundary wrong and every downstream number is precise to the gram and wrong by an operation.

Operational control is a GHG Protocol consolidation approach: a company reports 100% of emissions from operations it has authority to run, regardless of equity share. It sets the Scope 1 boundary.

What Operational Control Means

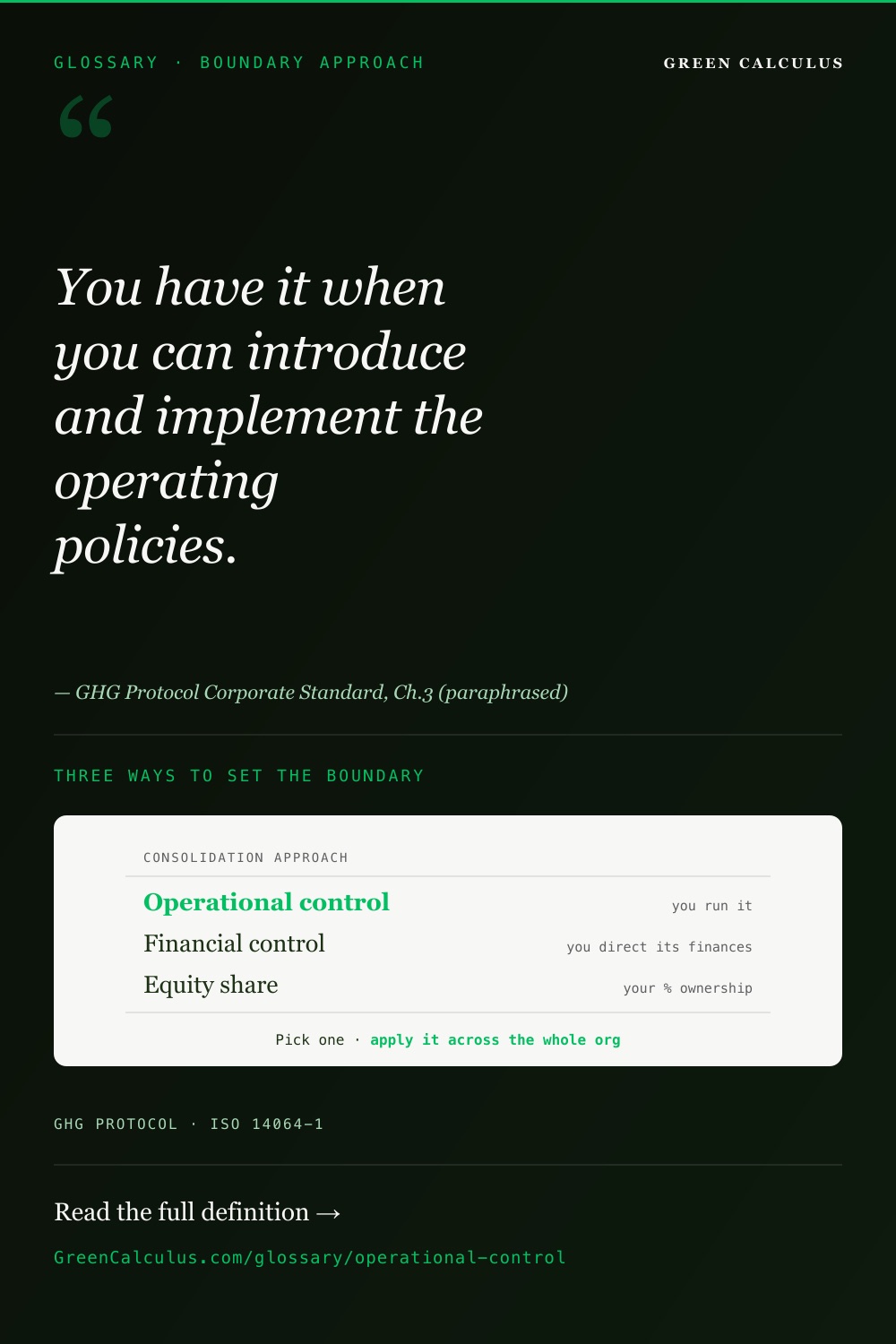

Operational control is one of the methods a company uses to draw its organisational boundary — the line that decides which operations it consolidates into its greenhouse gas inventory. Under the GHG Protocol Corporate Standard, a company has operational control over an operation when it (or one of its subsidiaries) has the full authority to introduce and implement the operation’s operating policies. It is one of two control-based approaches; the alternative, equity share, is ownership-based.

The defining feature is that operational control is about authority to run, not about ownership percentage and not about who carries the financial risk and reward. A company can hold operational control while owning a minority equity stake, and it can own a majority stake without holding operational control. That decoupling is the source of most boundary errors.

If your company has the authority to introduce and implement the operating policies of an operation — to decide how it is run day to day — you have operational control over it, and you consolidate 100% of that operation’s emissions. Holding a financial stake without that operating authority is not operational control.

The Three Consolidation Approaches

The GHG Protocol Corporate Standard offers two control-based approaches — operational control and financial control — alongside the ownership-based equity share approach. A company selects one and applies it consistently across the whole inventory. The choice does not change physical emissions; it changes which emissions appear in this company’s inventory.

| Approach | Basis | What you consolidate | Typical adopter |

|---|---|---|---|

| Operational control | Authority to set operating policy | 100% of emissions from operations you run; 0% from operations you don’t run | Most corporates — aligns with where mitigation action is actually taken |

| Financial control | Ability to direct financial & operating policy for economic benefit | 100% of emissions from financially controlled entities (broadly, those consolidated on the balance sheet) | Companies aligning the GHG boundary to the financial reporting boundary |

| Equity share | Percentage ownership / economic interest | Emissions in proportion to equity held (e.g. 40% stake → 40% of emissions) | Oil & gas, mining, JV-heavy portfolios where economic interest is the fairer lens |

Source: GHG Protocol Corporate Accounting and Reporting Standard, Chapter 3 (Organisational Boundaries). ISO 14064-1:2018 aligns with the same control / equity-share consolidation logic.

Operational control draws the boundary around the operations a company can actually change. The emissions inside the boundary are the ones management has the authority to reduce — which makes the inventory a more direct match to a decarbonisation plan than an equity-weighted view that includes operations someone else runs. It is also the boundary most consistent with how CSRD / ESRS E1 expects operational-level disclosure to be framed.

Applying the Operational Control Test

The single question is: does your company hold the authority to introduce and implement the operating policies of this operation? Ownership percentage, board seats, and profit share are evidence — but none of them is the test on its own. The decision table below maps the structures that come up most often.

| Structure | Who sets operating policy? | Operational control? | Consolidate |

|---|---|---|---|

| Wholly-owned subsidiary you run | You | Yes | 100% |

| Majority stake, you appoint management | You | Yes | 100% |

| Minority stake, but you are the named operator | You | Yes | 100% |

| Majority stake, partner is contractual operator | Partner | No | 0% |

| 50/50 JV, neither party runs it alone | Shared / JV management | Depends on the JV agreement | 0% or 100% |

| Asset leased to you, you operate it | You | Yes | 100% |

| Asset you own, leased out to a tenant who runs it | Tenant | No | 0% |

Decision logic derived from GHG Protocol Corporate Standard Chapter 3 and the GHG Protocol leased-assets guidance. The two 0% or 100% rows resolve only by reading the specific operating agreement — see §4.

Where It Gets Hard — Leased Assets, JVs, and Franchises

The clean cases — wholly-owned operations you run, third-party operations you don’t — almost never cause errors. Boundary mis-statements cluster in three structures where authority and ownership pull apart. These are the cases worth a deliberate determination rather than a default.

Leased assets

Treatment turns on the operating authority, not the lease’s accounting classification. If you lease an asset and run it, it falls inside an operational-control boundary as Scope 1. If you own an asset and lease it out to a tenant who runs it, it sits outside — the emissions become your Scope 3 (downstream leased assets).

Joint ventures

A JV resolves on the agreement, not the split. A 50/50 JV with a named operator gives that operator 100% under operational control and the other partner 0%. A jointly-operated JV where neither party can set policy alone may leave neither holding operational control — a case the GHG Protocol flags for explicit documentation.

Franchises

A franchisor typically sets brand and some operating standards but does not run the franchisee’s site. Under operational control the franchisor usually does not consolidate franchisee emissions — they become franchisor Scope 3 (franchises), while the franchisee reports them as its own Scope 1 and 2.

A company chooses one consolidation approach and applies it across the entire inventory — it cannot use operational control for the operations it likes and equity share for the rest. Mixing approaches between operations, or quietly switching approaches between reporting years without restating the base year, breaks comparability and is one of the fastest ways to fail assurance under ISO 14064-1 or ESRS E1. If the approach changes, the base year is recalculated.

How the Boundary Choice Sets Scope 1 vs Scope 3

The organisational boundary is logically prior to the scopes. You first decide which operations are inside the boundary; only then do emissions from those operations get classified as Scope 1, Scope 2, or Scope 3. The same physical emission can land in a different scope — or leave the inventory entirely — purely on the basis of where the boundary was drawn.

| Emission source | Inside operational-control boundary? | Scope |

|---|---|---|

| Fuel combustion in an operation you run | Yes | Scope 1 |

| Purchased electricity for an operation you run | Yes | Scope 2 |

| Emissions from an asset you own but lease out | No (tenant runs it) | Scope 3 (downstream leased assets) |

| Emissions from a JV you hold equity in but don’t operate | No | Scope 3 (investments) — or excluded, per agreement |

| Franchisee site emissions (you are franchisor) | No | Scope 3 (franchises) |

Scope assignment follows the GHG Protocol Corporate Standard once the boundary is fixed. Scope 2 treatment further splits into location- and market-based methods — see the Scope 2 electricity methodology and Scope 2 Guidance.

Why this mattersAn operation that is Scope 1 under operational control can become Scope 3 — or disappear from the inventory — under equity share. Targets, intensity metrics, and assurance scope all sit on top of this single boundary decision, which is why the GHG Protocol requires it to be stated explicitly and applied consistently.

Why the Choice Changes the Reported Total — a Worked Illustration

The clearest way to see the effect is to hold the operations fixed and vary only the consolidation approach. Consider a parent company, ParentCo, with three operations. The physical emissions never change — only the boundary does.

| Operation | Equity held | Who operates it | Gross emissions (t CO₂e) |

|---|---|---|---|

| A — wholly-owned plant, ParentCo runs it | 100% | ParentCo | 50,000 |

| B — JV, ParentCo is named operator | 30% | ParentCo | 40,000 |

| C — JV, partner is the operator | 60% | Partner | 30,000 |

Now consolidate the same three operations under each approach. The total ParentCo reports swings substantially:

| Operation | Operational control | Equity share |

|---|---|---|

| A — owned & operated (100% equity) | 50,000 | 50,000 |

| B — operated, 30% equity | 40,000 | 12,000 |

| C — not operated, 60% equity | 0 | 18,000 |

| ParentCo reported total | 90,000 | 80,000 |

Illustrative figures, hardcoded per Editorial Standards §9b — these are boundary-rule arithmetic, not MasterBrain values. Operational control captures 100% of B (operated, low equity) and 0% of C (not operated, high equity); equity share captures both in proportion to ownership. Same operations, different total, entirely from the boundary choice.

Three observations for practitioners:

- Operation B is the swing. ParentCo operates it on a 30% stake, so operational control pulls in the full 40,000 t while equity share takes only 12,000 t. This is the classic case where authority and ownership diverge.

- Operation C disappears under operational control. Despite a 60% equity majority, ParentCo doesn’t run it — so it leaves the Scope 1/2 boundary entirely and is reported as Scope 3 (investments) instead.

- Neither total is “right.” They answer different questions. Operational control answers “what can we directly reduce?”; equity share answers “what are we economically exposed to?” The standard requires you to pick one and disclose it, not to reconcile them.

Once the boundary is set, quantify what falls inside it — Scope 1 combustion and Scope 2 electricity for every operation you control.

Four Common Operational Control Mistakes

- Confusing operational control with majority ownership. The most common error — assuming a 60% or 100% equity stake automatically means operational control. It does not. If a partner is the contractual operator, the majority owner has 0% under operational control. Always read who holds operating authority, not who holds the larger stake.

- Applying different approaches to different operations. The boundary approach is chosen once and applied across the whole inventory. Consolidating the convenient operations under operational control and the rest under equity share produces a non-comparable total that fails assurance under ISO 14064-1. Pick one, document it, apply it everywhere.

- Getting leased assets backwards. Assets you lease in and operate are inside the boundary (Scope 1/2); assets you own and lease out are outside (Scope 3 downstream leased assets). Reporters frequently include owned-and-leased-out property in Scope 1 because they own it — which double-counts against the tenant’s own Scope 1 and overstates the boundary.

- Switching approaches without recalculating the base year. A change in consolidation approach is a structural change that requires base-year recalculation under the GHG Protocol. Switching from equity share to operational control between years — without restating the base year — makes a target look met or missed for reasons that have nothing to do with actual mitigation.

Related Terms, Standards, and Tools

Frequently Asked Questions

Operational control is one of the consolidation approaches in the GHG Protocol Corporate Standard for setting an organisation’s GHG inventory boundary. A company has operational control over an operation when it has full authority to introduce and implement that operation’s operating policies — in plain terms, when it runs the operation. Under this approach the company consolidates 100% of the operation’s emissions, regardless of how much equity it holds. It is the most widely used boundary approach because it aligns the inventory with the operations management can actually decarbonise.

All three are GHG Protocol approaches for deciding which operations a company consolidates. Operational control is based on authority to set operating policy — you report 100% of operations you run and 0% of those you don’t. Financial control is based on the ability to direct financial and operating policy for economic benefit, broadly tracking the financial-reporting consolidation boundary, also at 100%. Equity share is ownership-based — you report emissions in proportion to your equity stake, so a 40% holding means 40% of that operation’s emissions. A company picks one and applies it consistently across the whole inventory; the choice changes what appears in its inventory, not the physical emissions.

Yes — but only for operations you actually control, and it is all-or-nothing per operation. If your company holds the authority to set an operation’s operating policies, you consolidate 100% of that operation’s emissions even if you own a minority equity stake. If you do not hold that authority, you consolidate 0% — even with a majority stake. Operational control never apportions by percentage the way equity share does; each operation is either fully in or fully out of the Scope 1 and Scope 2 boundary. Operations that fall out are reported as Scope 3 where material.

Treatment follows operating authority, not the lease’s accounting classification. If you lease in an asset and operate it yourself, it sits inside your operational-control boundary and its emissions are Scope 1 (and Scope 2 for purchased electricity). If you own an asset and lease it out to a tenant who operates it, it falls outside your boundary and its emissions are your Scope 3 under downstream leased assets — while the tenant reports them as its own Scope 1 and 2. A common error is including owned-but-leased-out property in Scope 1 because of the ownership, which overstates the boundary and double-counts against the tenant.

There is no universally correct choice — the approaches answer different questions, and the standard requires you to select one, disclose it, and apply it consistently. Most corporates choose operational control because it draws the boundary around operations management can directly reduce, which aligns the inventory with a decarbonisation plan and with CSRD / ESRS E1 disclosure framing. Equity-share is common in oil & gas, mining, and JV-heavy portfolios where economic interest is the fairer lens. Whatever you choose, a later change in approach is a structural change that requires recalculating the base year under the GHG Protocol.

Set the boundary with operational control, then build the inventory inside it — direct combustion and purchased electricity for every operation you run.